This blog post explores some of the most successful omnichannel banking examples, showcasing how innovative banks have implemented this strategy. Through these real-world cases, we will uncover the key lessons and strategies that drive effective omnichannel banking solutions. Whether you’re a financial institution looking to enhance your customer experience or a curious reader interested in the future of banking, these omnichannel banking examples offer valuable insights into a transformative trend shaping the industry.

Table of Contents

Case Studies: Successful Omnichannel Banking Examples

These omnichannel banking examples showcase how innovative strategies can transform customer experiences, streamline operations, and ensure long-term growth. In this section, we delve into five comprehensive case studies that highlight successful omnichannel banking examples, shedding light on the challenges faced, strategies adopted, and outcomes achieved.

Case Study 1: Citibank

Citibank, a globally recognized financial institution, has long been at the forefront of banking innovation. As the financial sector embraced digital transformation, Citibank recognized the urgency of adapting to a rapidly changing landscape where customer expectations for seamless, integrated services were higher than ever. With millions of customers spread across numerous countries, the bank faced significant challenges in delivering consistent and personalized experiences. This case study delves into Citibank’s journey, highlighting how it became a standout among omnichannel banking examples by modernizing its services and overcoming operational inefficiencies.

By implementing a robust omnichannel strategy, Citibank was able to bridge the gap between its digital and physical channels, creating a cohesive ecosystem that catered to customer needs. This transformation not only improved customer satisfaction but also enhanced engagement and loyalty, positioning Citibank as a leader in omnichannel banking.

Background

Citibank’s journey toward omnichannel banking began with the acknowledgment that its traditional systems and fragmented customer interactions were no longer sufficient to meet the demands of a digitally savvy audience. While the bank had established itself as a trusted brand globally, the lack of integration between its channels created operational inefficiencies and inconsistent customer experiences.

- Challenges with Legacy Systems: Like many established financial institutions, Citibank relied heavily on legacy systems that were not designed for the seamless integration required in modern banking. These systems posed significant obstacles to unifying customer profiles and synchronizing data across various touchpoints. For instance, a customer’s transaction history on the mobile app was often inaccessible to branch staff, resulting in repetitive and fragmented service experiences.

- Fragmented Touchpoints: Citibank’s operations were spread across multiple channels, including mobile apps, online banking portals, physical branches, ATMs, and call centers. However, these touchpoints operated in silos, preventing customers from enjoying a consistent journey. A customer starting a transaction on the mobile app would often have to restart the process at a branch due to a lack of data integration. This disjointed experience was a source of frustration for customers and inefficiency for the bank.

- Demand for Modernization: Recognizing the shift in customer preferences toward digital-first interactions, Citibank identified the need to overhaul its services. The goal was to create a seamless experience that allowed customers to move effortlessly between channels while receiving personalized support. To achieve this, the bank needed to embrace advanced technologies such as artificial intelligence, machine learning, and real-time data synchronization.

Omnichannel Strategies

To address these challenges, Citibank implemented a comprehensive omnichannel strategy that unified its services and transformed its customer experience. By leveraging technology and adopting a customer-centric approach, the bank successfully modernized its operations and established itself as a leader among omnichannel banking examples.

- Unified Platform Integration

Citibank developed an integrated platform that connected its mobile app, online banking portal, and branch operations. This platform allowed customers to initiate transactions on one channel and complete them on another without disruption. For example, a customer could start a loan application on the mobile app, track its progress online, and finalize it in person at a branch, all without re-entering information or explaining their needs repeatedly.

This seamless integration ensured that customers experienced consistent service regardless of how they interacted with the bank. It also allowed Citibank to gather and consolidate customer data, enabling a deeper understanding of individual preferences and behaviors. - Artificial Intelligence and Machine Learning

Citibank harnessed the power of AI and machine learning to enhance its service offerings. These technologies were used to analyze customer data and provide personalized recommendations, such as tailored investment opportunities or savings plans. AI also powered Citibank’s virtual assistant, which could handle routine inquiries, guide customers through transactions, and escalate complex issues to human agents when necessary.

By leveraging AI, Citibank was able to deliver a level of personalization that resonated with customers, making them feel valued and understood. - Real-Time Data Synchronization

One of the key pillars of Citibank’s omnichannel strategy was the implementation of real-time data synchronization. This ensured that customer profiles were always up-to-date and accessible across all channels. Whether a customer interacted with a branch, called a support center, or used the mobile app, the bank’s staff and systems had immediate access to the latest information.

Real-time synchronization eliminated the inefficiencies caused by outdated or incomplete data, enabling smoother interactions and faster resolutions to customer queries. It also empowered branch and call center employees to provide personalized support based on the customer’s recent activities.

Results

Citibank’s adoption of these omnichannel strategies led to transformative results, solidifying its position as one of the most successful omnichannel banking examples.

- Enhanced Customer Satisfaction

The seamless integration of Citibank’s channels significantly improved the customer experience. Customers no longer faced the frustration of repeating information or navigating disjointed processes. Instead, they could transition effortlessly between digital and physical touchpoints, enjoying a consistent and personalized journey.

This convenience boosted customer satisfaction, as individuals felt that their time and preferences were respected. Whether managing accounts on the mobile app, seeking advice at a branch, or resolving issues through a call center, customers reported higher levels of satisfaction across the board. - Improved Customer Engagement

The use of AI and machine learning allowed Citibank to engage customers more effectively. Tailored recommendations and proactive alerts demonstrated the bank’s understanding of individual needs, fostering trust and loyalty. For example, customers appreciated receiving timely notifications about potential investment opportunities or reminders to avoid overdraft fees.

Additionally, the bank’s virtual assistant became a valuable tool for engaging customers, offering quick and accurate support for a wide range of inquiries. This not only improved the customer experience but also reduced the workload on human support staff. - Strengthened Brand Loyalty

By delivering a consistent and convenient experience, Citibank strengthened its reputation as a customer-centric institution. The bank’s commitment to innovation and service excellence resonated with its audience, leading to increased loyalty and retention. Customers who previously felt disconnected from the bank now viewed it as a reliable partner in managing their financial needs. - Operational Efficiency

The integration of Citibank’s services and the automation of routine tasks led to significant operational efficiencies. Real-time data synchronization reduced redundancies, while AI-powered tools streamlined customer interactions. These improvements allowed the bank to serve more customers with fewer resources, reducing costs while maintaining high service standards. - Competitive Advantage

Citibank’s success in implementing an omnichannel strategy gave it a distinct advantage over competitors that were slower to adapt. By positioning itself as a leader in digital transformation, the bank attracted tech-savvy customers and reinforced its brand as a forward-thinking institution.

Citibank’s journey toward omnichannel banking serves as an inspiring example for other financial institutions navigating the challenges of digital transformation. By addressing legacy system inefficiencies, unifying fragmented touchpoints, and leveraging advanced technologies, Citibank created a seamless and customer-centric banking experience.

This case study highlights the transformative potential of omnichannel strategies, showcasing how a traditional banking giant can adapt to the demands of the modern era. As one of the most compelling omnichannel banking examples, Citibank’s story offers valuable insights for banks aiming to enhance their services and thrive in an increasingly competitive landscape.

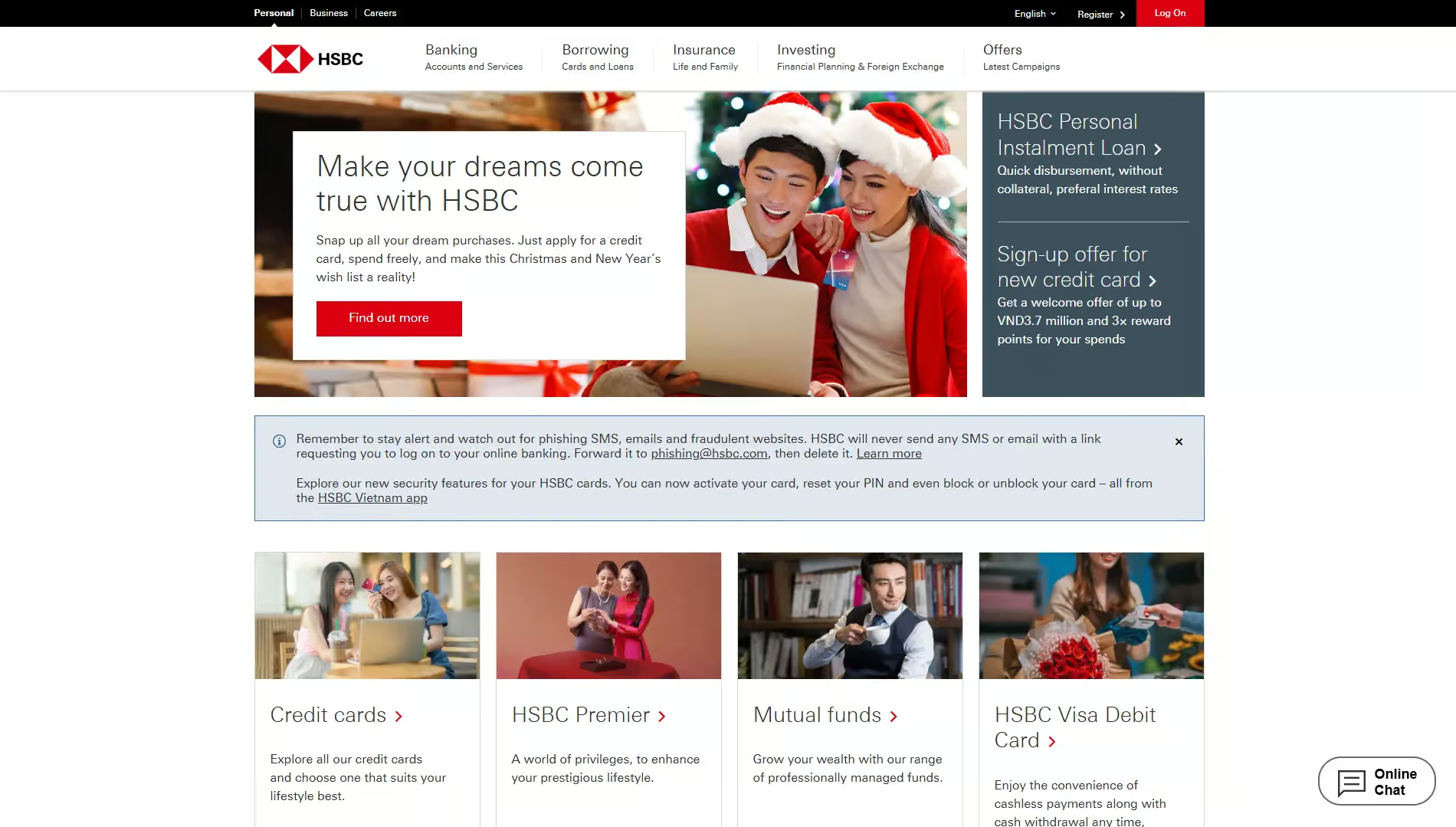

Case Study 2: HSBC

HSBC is a prime example of a financial institution that has successfully leveraged omnichannel banking to meet the dynamic needs of its global customer base. Operating in numerous markets worldwide, HSBC faced the challenge of catering to diverse customer demographics while maintaining a consistent and cohesive banking experience.

Through innovative strategies and a customer-centric approach, HSBC emerged as one of the most remarkable omnichannel banking examples, seamlessly integrating physical and digital channels to deliver exceptional services.

Background

As a multinational bank, HSBC serves customers across varying cultural, economic, and regulatory landscapes. This diversity posed significant challenges in unifying its operations and meeting the expectations of its global clientele. The need to address these challenges became apparent as customer preferences shifted toward digital platforms and seamless banking experiences.

- Global Operations and Diverse Customer Needs: HSBC’s extensive global footprint exposed it to a wide range of customer expectations. In some markets, customers prioritized digital convenience, while others valued the personalized assistance offered by physical branches. Balancing these preferences while adhering to local regulatory frameworks became a critical challenge.

- Accessibility and Cross-Border Challenges: HSBC’s customer base included expatriates, multinational corporations, and frequent travelers who required reliable and accessible cross-border banking services. However, inconsistencies in service delivery and limited integration across regions often created frustrations for customers seeking seamless global banking solutions.

- Demand for Digital Transformation: The growing reliance on digital banking, accelerated by technological advancements and changing customer habits, prompted HSBC to revamp its services. Customers increasingly sought mobile-first solutions that allowed them to manage their finances on the go. HSBC recognized the need to modernize its digital and physical channels to remain competitive and relevant.

Omnichannel Strategies

To address these challenges, HSBC implemented a comprehensive omnichannel banking strategy that prioritized customer convenience, technological innovation, and global accessibility. These initiatives positioned HSBC as one of the most impactful omnichannel banking examples in the industry.

- Mobile-First Approach

HSBC adopted a mobile-first strategy, recognizing that smartphones were becoming the primary medium for banking interactions. The bank enhanced its mobile app to include features such as real-time account management, international transfers, and secure communication with banking representatives. By doing so, HSBC ensured that its customers could access essential banking services anytime and anywhere.

The app’s design emphasized simplicity and usability, catering to a wide range of customers, from tech-savvy millennials to older generations. Key functionalities, such as biometric authentication and AI-driven support, were introduced to enhance security and customer engagement. - Enhanced Branch Experiences

While focusing on digital transformation, HSBC also revitalized its physical branches to complement its online services. The bank introduced augmented reality (AR) tools in select branches, allowing customers to visualize complex financial products and investment scenarios interactively. This technology made financial planning more accessible and engaging, bridging the gap between traditional banking and digital innovation.

Additionally, HSBC integrated self-service kiosks and digital displays in branches, enabling customers to perform routine transactions independently while reserving in-person interactions for more complex needs. These enhancements ensured that branches remained a vital part of the omnichannel ecosystem. - Global Transaction Platform

HSBC developed a unified global transaction platform to simplify cross-border banking. This platform allowed customers to manage multiple accounts in different countries, execute international transfers with real-time exchange rates, and access consolidated financial summaries. By integrating this platform into its mobile and online channels, HSBC provided a consistent and hassle-free experience for customers navigating global finances.

This feature proved particularly valuable for corporate clients and expatriates, who frequently deal with cross-border transactions and currency exchanges. The platform’s intuitive interface and real-time capabilities positioned HSBC as a leader in global financial services.

Results

The implementation of these strategies resulted in significant improvements across multiple dimensions of HSBC’s operations, reinforcing its status as one of the most successful omnichannel banking examples.

- Improved Customer Satisfaction

HSBC’s commitment to delivering consistent and accessible services across all channels resonated with its customers. The ability to transition seamlessly between mobile apps, branches, and online platforms enhanced convenience, leading to higher satisfaction rates. Customers appreciated the intuitive design of the mobile app, the informative branch experiences, and the reliability of the global transaction platform. - Increased Trust and Engagement

Innovative in-branch tools, such as AR and self-service kiosks, demonstrated HSBC’s dedication to staying at the forefront of banking technology. These advancements deepened customer trust, as they perceived HSBC as a forward-thinking institution. Personalized services, enabled by integrated customer data, further strengthened engagement and loyalty. - Leadership in Omnichannel Banking

HSBC’s efforts established it as a benchmark for omnichannel banking excellence. The bank’s ability to navigate the complexities of operating in diverse markets while maintaining a unified customer experience inspired other financial institutions to follow suit. HSBC’s approach demonstrated the scalability and adaptability of omnichannel banking solutions in a global context. - Operational Efficiency and Cost Savings: By integrating digital tools and automating routine processes, HSBC improved its operational efficiency. The enhanced mobile and online platforms reduced reliance on manual interventions, streamlining customer support and administrative tasks. This efficiency translated into cost savings, allowing HSBC to reinvest in further innovation.

- Stronger Brand Equity

HSBC’s omnichannel strategy not only improved customer experiences but also strengthened its brand image as a global leader in financial services. The bank’s ability to balance traditional and digital banking needs solidified its reputation as a reliable and innovative institution.

HSBC’s journey showcases how omnichannel banking examples can transform the way financial institutions engage with customers and address operational challenges. By adopting a mobile-first approach, enhancing branch experiences, and developing a robust global transaction platform, HSBC delivered a cohesive and customer-centric banking experience.

This case study highlights the importance of integrating digital and physical channels, leveraging advanced technologies, and prioritizing global accessibility to create a truly omnichannel ecosystem. HSBC’s success serves as a blueprint for other banks aiming to achieve excellence in omnichannel banking, proving that a customer-first mindset and innovative strategies can drive growth and loyalty in today’s competitive financial landscape.

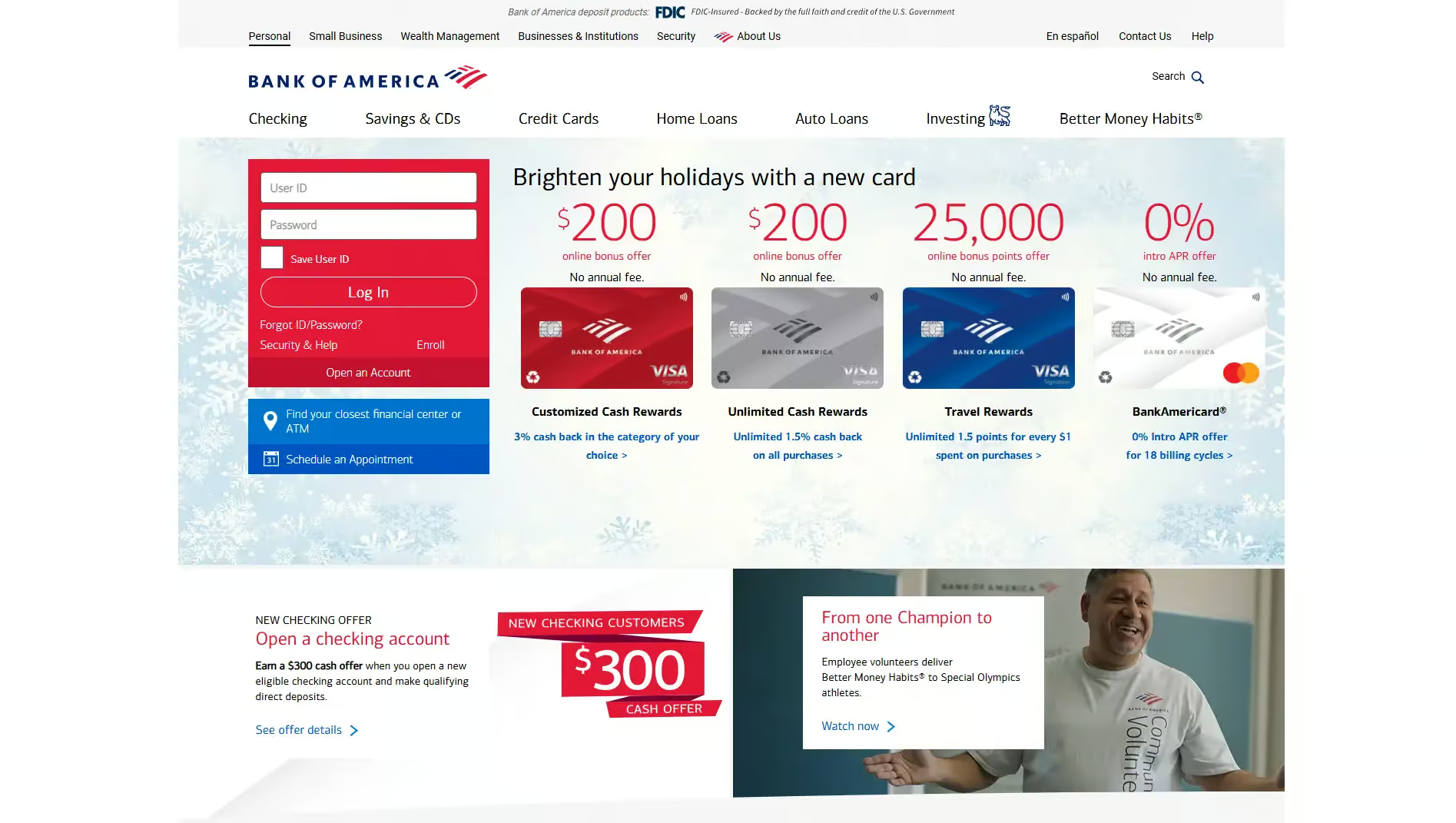

Case Study 3: Bank of America

Bank of America is one of the most prominent financial institutions in the United States, known for its commitment to innovation and customer-centric services. As the banking landscape shifted towards digitalization, Bank of America recognized the need to adapt to evolving customer expectations.

With a diverse customer base spanning different age groups and technological preferences, the bank set out to create an integrated system that offered accessibility and convenience without sacrificing the personal touch that customers valued. Through its groundbreaking strategies, Bank of America became one of the most notable omnichannel banking examples, showcasing how a well-designed approach can drive customer satisfaction and engagement.

Background

Bank of America’s transition to an omnichannel banking model was driven by its understanding of the changing preferences of its customers. The rise of smartphones and social media platforms, coupled with increasing expectations for on-demand services, reshaped how customers interacted with their financial institutions. While younger demographics leaned heavily on digital tools, older customers often required a blend of traditional and digital options. Balancing these needs became a key focus for Bank of America.

- Preference for Digital Interactions: Bank of America observed a growing trend among its customers, particularly younger demographics, favoring digital interactions over traditional banking methods. Mobile apps, online portals, and social media platforms became the preferred channels for tasks like checking account balances, making payments, and even seeking financial advice. This shift underscored the importance of enhancing digital offerings to meet customers where they were most active.

- Inclusivity Across Demographics: Despite the surge in digital preferences, Bank of America acknowledged that not all customers had the same level of technological proficiency. Many older customers, as well as those in rural areas, still relied on physical branches and in-person support. The bank’s goal was to ensure that its services were inclusive, catering to customers across all age groups and technological skill levels. By creating a seamless integration between physical and digital channels, Bank of America aimed to bridge the gap between traditional and modern banking.

- Reducing Friction While Maintaining Personalization: One of the bank’s core objectives was to minimize friction in customer interactions. Lengthy processes, repetitive information requests, and lack of personalization often frustrated customers and detracted from their experience. Bank of America sought to eliminate these pain points by creating a unified system that streamlined processes and maintained a personalized approach. This balance was critical to retaining its reputation as a customer-focused institution.

Omnichannel Strategies

Bank of America implemented a series of innovative strategies to achieve its vision of seamless, accessible, and personalized banking. These initiatives positioned the bank as a leader among omnichannel banking examples, illustrating how financial institutions can leverage technology to enhance the customer experience.

- Launch of “Erica,” an AI-Powered Virtual Assistant

Designed to provide instant support across digital platforms, Erica quickly became a cornerstone of the bank’s omnichannel strategy.

Erica was equipped with advanced AI and natural language processing, enabling it to understand and respond to customer queries in real time. Customers could interact with Erica via the mobile app, receiving assistance with tasks like transferring funds, checking credit scores, and setting financial goals. The assistant also provided proactive alerts and personalized recommendations based on customer activity, such as suggesting ways to save on fees or offering reminders about upcoming bill payments.

Erica reduced the reliance on traditional customer service channels, such as call centers, by resolving routine queries efficiently. For more complex issues, Erica seamlessly redirected customers to human agents, ensuring a smooth transition. This blend of automation and human interaction enhanced the overall customer experience. - Integration with Social Media Channels

Recognizing the importance of engaging customers where they spent significant time, Bank of America integrated its banking services with popular social media platforms. Customers could connect with the bank via Facebook and Twitter to access support, receive updates, and interact with personalized content.

By establishing a presence on social media, the bank not only enhanced accessibility but also built stronger relationships with customers. Social media platforms allowed the bank to share educational resources, promote new products, and address customer concerns in a timely manner. This approach resonated particularly well with younger customers, who appreciated the convenience of accessing support without leaving their preferred platforms.

The integration of social media with other banking channels ensured a seamless customer journey. For example, customers who initiated a conversation on social media could continue the interaction through the mobile app or in a branch, with all relevant information readily available to bank representatives. - Consistent Messaging and Branding Across Channels

Bank of America prioritized consistency in its messaging and branding to create a cohesive experience across all touchpoints. Whether customers interacted with the bank via branches, the mobile app, online portals, or social media, they encountered the same tone, visuals, and messaging.

This unified approach reinforced the bank’s commitment to reliability and professionalism. Customers were reassured by the familiarity of the brand, regardless of the channel they used, which contributed to building trust and loyalty.

Consistent messaging was complemented by a robust integration of customer data across channels. For instance, a customer discussing mortgage options at a branch could later receive a follow-up email summarizing their options, with the same information accessible on their online banking dashboard. This level of continuity demonstrated the bank’s ability to deliver personalized service at every stage of the customer journey.

Results

Bank of America’s omnichannel strategies yielded significant results, solidifying its position as a leading example of how financial institutions can thrive in the digital age.

- Praise for “Erica”

Customers widely lauded Erica for its intuitive interface and ability to resolve queries quickly. The virtual assistant’s proactive recommendations and real-time support made it an invaluable tool for managing finances. Erica’s success highlighted the potential of AI in enhancing customer interactions while reducing the burden on traditional support channels. - Enhanced Accessibility Across Channels

The integration of social media and consistent branding across platforms made Bank of America’s services more accessible to a broader audience. Customers could choose the channels that suited their preferences and still enjoy a seamless and personalized experience. This flexibility boosted overall customer satisfaction and loyalty. - Increased Digital Adoption While Retaining Physical Engagement

By offering robust digital solutions without neglecting physical branches, Bank of America achieved a balance that appealed to customers across demographics. Digital banking adoption rates increased significantly, with more customers utilizing the mobile app and online portals for day-to-day tasks. At the same time, physical branches remained an integral part of the customer experience, serving as a trusted resource for complex transactions and personalized advice. - Operational Efficiency and Cost Savings

The automation of routine queries through Erica and the integration of digital channels streamlined operations, reducing the need for manual intervention. This efficiency allowed Bank of America to lower costs while maintaining high standards of service. - Strengthened Customer Loyalty

The bank’s commitment to personalization, accessibility, and consistency resonated deeply with customers. By eliminating friction and meeting customers where they were, Bank of America strengthened relationships and fostered long-term loyalty.

Bank of America’s journey demonstrates how a well-executed omnichannel strategy can transform the customer experience while driving operational success. By launching Erica, integrating social media, and maintaining consistent branding across channels, the bank created a seamless and customer-centric ecosystem. This case study serves as a powerful example of how omnichannel banking examples can inspire financial institutions to adapt to changing customer expectations and thrive in a competitive landscape.

As one of the most compelling omnichannel banking examples, Bank of America’s approach highlights the importance of innovation, inclusivity, and personalization in building a modern banking experience. Other financial institutions can look to this success story as a blueprint for delivering exceptional value in an increasingly digital world.

Case Study 4: DBS Bank

DBS Bank, headquartered in Singapore, has long been recognized as a trailblazer in the banking industry, particularly in the Asia-Pacific region. By embracing digital transformation early on, DBS positioned itself as a leader in innovation and customer-centric services. As the demand for seamless and sustainable banking solutions grew, DBS leveraged its technological expertise to implement a comprehensive omnichannel strategy.

This approach enabled the bank to integrate its physical and digital channels, delivering consistent, efficient, and personalized services to its customers. Among the many omnichannel banking examples, DBS Bank stands out for its commitment to sustainability and technological innovation, setting new benchmarks for the industry.

Background

DBS Bank’s transition to an omnichannel banking model was driven by its vision to become the “best bank in the world” while addressing inefficiencies in its existing operations. The bank’s strategy was shaped by three key challenges:

- A Pioneer in Digital Banking: DBS Bank has always been at the forefront of digital banking in the Asia-Pacific region, pioneering innovative solutions that catered to the evolving needs of its customers. However, as customer expectations continued to rise, the bank faced the challenge of maintaining its leadership by offering an integrated, omnichannel experience that blended digital convenience with personalized services.

- Challenges with Paper-Based Processes: Like many traditional banks, DBS initially relied on paper-based processes for branch operations, which were time-consuming and inefficient. Customers often faced delays in completing routine tasks, such as account opening or loan applications, due to the extensive paperwork required. This inefficiency not only impacted customer satisfaction but also increased operational costs.

- Alignment with Sustainability Goals: DBS Bank recognized the importance of aligning its operations with global sustainability goals. Paper-based processes and traditional branch setups contradicted the bank’s commitment to environmental responsibility. The need to adopt eco-friendly practices while enhancing customer experiences became a critical driver for change.

By addressing these challenges, DBS aimed to transform its banking solutions, reduce inefficiencies, and deliver a unified experience across all customer touchpoints.

Omnichannel Strategies

To achieve its vision, DBS Bank implemented a series of innovative strategies that redefined how customers interacted with its services. These initiatives positioned DBS as one of the most notable omnichannel banking examples in the industry.

- Transition to Paperless Branches

DBS Bank revolutionized its branch operations by transitioning to a paperless model. This initiative involved integrating digital kiosks, tablets, and e-forms into branch workflows. Customers could complete tasks such as account opening, loan applications, and document submissions digitally, eliminating the need for physical paperwork.

Digital kiosks allowed customers to perform routine banking tasks independently, reducing wait times and freeing up branch staff to focus on more complex needs. E-forms replaced traditional paper forms, enabling faster processing and greater accuracy.

The paperless model aligned with DBS’s sustainability goals by significantly reducing paper consumption. This initiative also enhanced the bank’s reputation as an environmentally conscious organization, resonating with customers who valued sustainable practices. - Utilization of AI and Data Analytics

DBS leveraged AI and advanced data analytics to deliver real-time financial insights and personalized recommendations to its customers. These technologies played a central role in enhancing the bank’s omnichannel offerings.

AI-powered tools analyzed customer data to provide real-time updates on account activity, spending patterns, and investment performance. Customers received proactive alerts and suggestions tailored to their financial goals, such as reminders to save or opportunities to invest.

Data analytics enabled the bank to offer customized solutions based on individual customer needs. For instance, customers planning a major purchase could receive tailored loan offers, while those nearing retirement might be advised on appropriate savings plans. This level of personalization deepened customer engagement and loyalty. - Consistent User Experience Across Channels

DBS Bank prioritized delivering a unified experience across all its touchpoints, including mobile apps, ATMs, and branch interactions. This consistency ensured that customers could transition seamlessly between channels without encountering disruptions.

The DBS mobile app was designed to offer a user-friendly interface with features such as account management, fund transfers, bill payments, and financial planning tools. The app also integrated AI-driven support, enabling customers to receive assistance without visiting a branch.

Whether customers interacted with DBS via the mobile app, ATMs, or branches, they encountered the same design, messaging, and functionality. For example, a customer initiating a transaction on the app could complete it at an ATM or receive support at a branch without restarting the process. This seamless integration fostered trust and convenience.

Results

DBS Bank’s omnichannel strategies delivered transformative results, underscoring its status as a leading example of how financial institutions can effectively implement omnichannel banking solutions.

- Faster and More Efficient Services

The transition to paperless branches significantly reduced the time required for routine transactions. Customers no longer had to fill out lengthy paper forms or wait for manual approvals, resulting in a faster and more efficient experience. The use of digital kiosks and e-forms streamlined workflows, allowing the bank to serve more customers in less time. - Strengthened Customer Loyalty

By utilizing AI and data analytics to provide personalized recommendations, DBS deepened its relationships with customers. Proactive financial advice demonstrated the bank’s understanding of individual needs, fostering trust and loyalty. Customers appreciated the convenience of receiving tailored solutions, whether they were planning for retirement or managing daily expenses. - Operational Efficiency and Cost Savings

The adoption of digital tools and automated processes reduced the bank’s reliance on manual workflows, leading to significant cost savings. Real-time data synchronization minimized errors and redundancies, further enhancing operational efficiency. The paperless model also reduced expenses associated with printing, storage, and document management. - Alignment with Sustainability Goals

DBS’s transition to paperless operations demonstrated its commitment to environmental sustainability. The initiative not only reduced the bank’s carbon footprint but also positioned it as a socially responsible organization. This alignment with sustainability resonated with customers and stakeholders, enhancing the bank’s brand image.

DBS Bank’s success in implementing an omnichannel banking strategy highlights the transformative potential of integrating digital innovation with customer-centric services. By addressing inefficiencies, leveraging advanced technologies, and aligning with sustainability goals, DBS created a seamless and eco-friendly banking experience that set new standards for the industry.

This case study exemplifies how omnichannel banking examples can inspire financial institutions to rethink traditional models and embrace change. DBS’s journey underscores the importance of innovation, consistency, and sustainability in building a modern banking ecosystem that meets the evolving needs of customers. As a pioneer in digital banking, DBS Bank serves as a shining example of how to thrive in a competitive and rapidly changing landscape.

Case Study 5: Wells Fargo

Wells Fargo, one of the most established financial institutions in the United States, has a long-standing reputation for prioritizing customer satisfaction. Recognizing the shift towards digital-first interactions, Wells Fargo embarked on a mission to enhance its banking experience through a robust omnichannel strategy.

This transformation aimed to provide customers with seamless access to banking services across digital platforms and physical branches. As one of the most significant omnichannel banking examples in the industry, Wells Fargo’s approach combined innovative technologies, personalized engagement, and a focus on self-service solutions to meet the evolving needs of its diverse clientele.

Background

Wells Fargo’s journey toward omnichannel banking was rooted in its commitment to staying competitive in a rapidly changing financial landscape. The bank faced several challenges that necessitated a reevaluation of its customer experience and operational efficiency.

- Commitment to a Customer-Centric Approach: Wells Fargo has always been known for its customer-centric philosophy, emphasizing personalized service and relationship banking. However, with the rise of digital banking, customers began to expect the same level of personalization and support across online and mobile platforms. To maintain its competitive edge, the bank needed to innovate while preserving its traditional customer-focused values.

- Challenges with Siloed Customer Data: Like many legacy institutions, Wells Fargo struggled with siloed customer data spread across various departments and platforms. This lack of integration led to inconsistent customer experiences. For example, a customer’s transaction history on the mobile app might not be accessible to branch employees, forcing customers to repeat information and disrupting the continuity of their banking experience.

- Empowering Customers with Self-Service Options: Wells Fargo recognized a growing demand among its customers for greater autonomy in managing their finances. Self-service tools, such as loan calculators and automated savings plans, were increasingly sought after by tech-savvy customers. At the same time, the bank aimed to enhance the quality of support for those requiring personalized assistance. Balancing these priorities became a critical focus for Wells Fargo’s omnichannel strategy.

Omnichannel Strategies

Wells Fargo implemented a series of targeted strategies to address these challenges and deliver a cohesive, customer-focused omnichannel banking experience. These initiatives exemplify how omnichannel banking examples can bridge the gap between traditional banking practices and modern digital demands.

- Unified Customer Profile System

One of the foundational elements of Wells Fargo’s omnichannel transformation was the creation of a unified customer profile system. This system centralized customer data, enabling seamless data sharing across digital platforms and physical branches.

By consolidating customer information into a single, accessible database, Wells Fargo ensured that every touchpoint—whether a mobile app, call center, or branch—had access to the same up-to-date customer data. This eliminated redundancies, such as customers needing to repeat their account details or transaction histories across different channels.

Branch employees and call center representatives could now access detailed customer profiles, allowing them to provide more informed and personalized assistance. This integration also streamlined complex processes, such as loan applications or dispute resolutions, resulting in faster and more efficient service. - Advanced Self-Service Tools

To empower customers and reduce reliance on manual support, Wells Fargo enhanced its mobile and online platforms with a suite of self-service tools. These tools catered to a wide range of financial needs, offering customers greater autonomy and convenience.

The bank introduced user-friendly loan calculators that allowed customers to explore borrowing options and calculate repayment schedules independently. Similarly, automated savings plans enabled customers to set financial goals and track their progress in real time, fostering greater financial literacy and control.

The Wells Fargo mobile app was upgraded to include features like bill payments, fund transfers, and detailed account insights. The app’s intuitive design and AI-driven guidance ensured that customers of all technological skill levels could navigate it with ease. - Proactive Customer Engagement

Wells Fargo adopted a proactive approach to customer engagement, using data analytics and AI to anticipate customer needs and deliver personalized interactions.Customers received tailored alerts about account activity, such as low balance warnings or potential overdrafts. Additionally, the bank provided targeted offers, such as promotional rates on loans or credit cards, based on individual spending patterns and financial goals.

The bank utilized digital channels like email and push notifications to keep customers informed and engaged. These communications were timely, relevant, and personalized, reinforcing Wells Fargo’s commitment to customer satisfaction.

Results

Wells Fargo’s omnichannel strategies delivered significant benefits, transforming the customer experience and driving operational improvements. These results demonstrate the effectiveness of its approach and solidify its place among the most successful omnichannel banking examples.

- Increased Customer Satisfaction

The unified customer profile system and self-service tools made banking easier and more accessible for Wells Fargo’s customers. The ability to complete routine tasks independently while still having access to personalized support when needed significantly improved the overall customer experience. Customers reported higher levels of satisfaction due to the bank’s ability to meet their needs efficiently and consistently. - Improved Customer Retention

The personalized engagement strategies employed by Wells Fargo helped foster deeper relationships with its customers. Proactive alerts and tailored offers demonstrated the bank’s understanding of individual customer needs, creating a sense of trust and loyalty. As a result, the bank saw a reduction in customer attrition rates and an increase in long-term retention. - Operational Savings and Efficiency

By automating routine processes and empowering customers with self-service tools, Wells Fargo reduced its reliance on manual customer support. This not only lowered operational costs but also freed up resources to focus on more complex and high-value interactions. The centralized data system further streamlined operations, minimizing errors and redundancies. - A Balanced Approach to Digital and Physical Channels

While Wells Fargo invested heavily in its digital platforms, it did not neglect its physical branches. The integration of digital tools with branch operations ensured that customers received a seamless experience, regardless of their preferred channel. This balance allowed the bank to cater to a diverse customer base, including those who valued traditional banking methods.

Wells Fargo’s journey toward omnichannel banking exemplifies how financial institutions can effectively adapt to the demands of the digital age while preserving their core values. By addressing challenges such as siloed data and evolving customer expectations, the bank created a cohesive and customer-focused ecosystem. Its strategies, including the unified customer profile system, advanced self-service tools, and proactive engagement initiatives, positioned Wells Fargo as one of the most compelling omnichannel banking examples in the industry.

This case study underscores the importance of innovation, personalization, and integration in modern banking. By empowering customers, streamlining operations, and delivering consistent experiences across channels, Wells Fargo demonstrated that omnichannel banking is not just a strategy—it is a necessity for long-term success in a competitive financial landscape. Financial institutions looking to enhance their services can draw valuable lessons from Wells Fargo’s approach, proving that a customer-centric focus and technological innovation can drive meaningful results.

Key Lessons from the Case Studies

Omnichannel banking examples from industry leaders like Citibank, HSBC, Bank of America, DBS Bank, and Wells Fargo offer valuable insights into what it takes to successfully implement a unified, customer-focused banking strategy. These case studies highlight the importance of integrating technology, understanding customer needs, and maintaining consistency across channels. In this section, we explore the key lessons that financial institutions can glean from these omnichannel banking examples, providing actionable insights for banks striving to enhance their operations and customer experiences.

Insights for Banks Starting their Omnichannel Journey

The omnichannel banking examples of industry leaders highlight the importance of a strategic, customer-focused approach. For banks starting their omnichannel journey, understanding customer needs, investing in foundational technology, and adopting a phased implementation strategy are critical steps to success. This section explores these insights in depth, providing actionable advice for financial institutions aiming to transform their operations and customer experiences.

Understand Customer Needs and Preferences

One of the most important lessons from successful omnichannel banking examples is the necessity of deeply understanding customer needs and preferences. A customer-first mindset ensures that the solutions a bank implements resonate with its audience and enhance the overall experience.

- Conduct Detailed Customer Segmentation

To effectively meet customer expectations, banks must perform in-depth segmentation to categorize their audience based on demographics, behaviors, and preferences. For instance, younger customers may prefer mobile-first services with advanced self-service tools, while older demographics might value personalized assistance in branches. By tailoring strategies to each segment, banks can create solutions that cater to diverse needs.

HSBC’s omnichannel banking example demonstrates how understanding its global customer base allowed it to design services that seamlessly bridged digital and physical touchpoints, ensuring accessibility for both tech-savvy and traditional customers. - Leverage Surveys, Feedback Loops, and Data Analytics

Capturing insights into customer behavior is vital for refining omnichannel strategies. Banks can use tools like surveys and feedback loops to gather qualitative data about customer pain points and expectations. Pairing this with quantitative insights from data analytics provides a comprehensive view of customer behavior.

Citibank, for example, leveraged AI and data analytics to gain insights into customer preferences, enabling the delivery of tailored financial recommendations through its unified platforms. Such strategies reinforce the importance of listening to customers and using data to inform decisions.

Start with Foundational Technology

The success of many omnichannel banking examples hinges on the implementation of robust foundational technologies. These systems provide the infrastructure needed to unify customer profiles, integrate touchpoints, and enable seamless experiences.

- Implement Core Systems Like CRM and Data Integration Platforms

A CRM system and data integration platform are essential tools for any bank embarking on an omnichannel transformation. These systems centralize customer data, ensuring that all touchpoints—from mobile apps to call centers—have access to consistent and up-to-date information.

Wells Fargo’s success in creating a unified customer profile system is a prime omnichannel banking example of how foundational technology can eliminate silos and enhance service consistency. This investment enabled the bank to deliver a cohesive experience across digital and physical channels. - Prioritize Real-Time Synchronization

Foundational technology must allow for real-time synchronization of customer interactions. This capability ensures that actions taken on one channel (e.g., a mobile app) are immediately reflected on others (e.g., branch systems or call center platforms). Real-time synchronization not only improves operational efficiency but also reduces customer frustration by eliminating redundant processes.

DBS Bank’s integration of AI-driven tools and real-time data synchronization showcases how advanced technology can create a unified framework for delivering personalized and consistent banking experiences.

Adopt a Phased Approach

Implementing an omnichannel strategy is a complex process that requires careful planning and execution. Many omnichannel banking examples emphasize the value of adopting a phased approach, starting with high-impact channels and iteratively refining strategies as the rollout progresses.

- Focus on High-Impact Channels First

Banks should identify the channels that offer the greatest potential for improving customer experiences and begin their transformation there. For example, mobile banking and branch services are often the most critical touchpoints for customers, making them ideal starting points. Once these channels are optimized, banks can expand to include others, such as ATMs, online portals, and call centers.

Bank of America’s launch of Erica, its AI-powered virtual assistant, is a notable omnichannel banking example of focusing on a high-impact channel. By enhancing its mobile platform first, the bank was able to deliver immediate value to customers while laying the groundwork for future channel integration. - Monitor Customer Response and Refine Strategies

A phased approach allows banks to gather feedback and assess the effectiveness of their omnichannel initiatives at each stage. By closely monitoring customer responses, banks can identify areas for improvement and refine their strategies before expanding to additional channels.

Citibank’s iterative approach to integrating digital and physical channels highlights the importance of continuous improvement. By testing and refining its solutions during each phase of implementation, the bank ensured a smoother transition and better alignment with customer expectations.

The lessons from these omnichannel banking examples provide a roadmap for banks starting their journey toward creating a unified and customer-focused ecosystem. By understanding customer needs and preferences, investing in foundational technology, and adopting a phased approach, banks can overcome challenges and deliver seamless, personalized experiences. These insights demonstrate that success in omnichannel banking is not only achievable but also essential for staying competitive in a rapidly evolving financial landscape.

Best Practices in Omnichannel Banking

The case studies of leading financial institutions offer rich insights into what makes an omnichannel strategy successful. By analyzing these omnichannel banking examples, we can identify best practices that can guide banks in delivering seamless, customer-focused services. These practices include integrating channels cohesively, leveraging advanced analytics and AI, and investing in employee training to ensure consistent and personalized customer interactions.

Seamless Integration Across Channels

Seamless channel integration is one of the foundational pillars of successful omnichannel banking. The most effective omnichannel banking examples demonstrate that providing a consistent customer experience across all platforms is key to fostering trust and satisfaction.

- Consistency in Branding, Messaging, and User Interfaces

Customers expect familiarity when interacting with a bank across multiple touchpoints. Whether they access their accounts through a mobile app, website, or branch, the branding, messaging, and user interface should be cohesive. Consistent design and communication not only reinforce a bank’s brand identity but also create a sense of reliability and professionalism.

For instance, Wells Fargo exemplified this best practice by maintaining uniform branding and messaging across its mobile app, online portal, and physical branches. This consistency reassures customers that they are receiving the same quality of service regardless of the channel they choose. - Real-Time Updates Across Channels

One of the hallmarks of successful omnichannel banking examples is the ability to synchronize customer actions across channels in real-time. Whether it’s completing a transaction, updating contact information, or applying for a loan, customers expect their actions on one platform to be instantly reflected across all others.

Citibank’s unified platform is a standout example of real-time integration. Customers could begin a transaction on the mobile app, continue it on the online portal, and finalize it at a branch without any disruptions. This level of integration eliminates redundancies and enhances the customer experience.

Leverage Advanced Analytics and AI

The effective use of advanced analytics and AI is a recurring theme in successful omnichannel banking examples. These technologies enable banks to deliver proactive, personalized, and efficient services that resonate with modern customers.

- Predictive Analytics for Anticipating Customer Needs

Predictive analytics is a powerful tool that allows banks to anticipate customer needs based on their behavior and transaction history. By analyzing patterns, banks can identify opportunities to offer relevant products or services before the customer even asks. For example, if a customer consistently saves a portion of their income, the bank could proactively recommend a higher-interest savings account or an investment product.

HSBC’s use of data analytics to deliver tailored financial advice is a prime example of this best practice. The bank leveraged customer data to provide personalized recommendations, ensuring that its services aligned with individual financial goals. - AI-Driven Tools for Personalization and Efficiency

AI-powered tools, such as chatbots and virtual assistants, have revolutionized how banks interact with customers. These tools can handle routine queries, guide users through transactions, and escalate complex issues to human agents when necessary. By blending automation with human support, banks can enhance both efficiency and personalization.

Bank of America’s “Erica” virtual assistant is a leading example of how AI can elevate the omnichannel experience. Erica’s ability to provide instant, accurate support across digital platforms has made it a valuable asset for the bank, improving customer engagement and satisfaction.

Invest in Employee Training

While technology is a cornerstone of omnichannel banking, human interaction remains a critical component of the customer experience. Successful omnichannel banking examples highlight the importance of equipping employees with the skills and tools they need to deliver consistent, high-quality service.

- Training for Seamless Customer Query Handling

In an omnichannel environment, customers may start their journey on one platform and seek support on another. For example, a customer might apply for a credit card online and later visit a branch for follow-up questions. Employees must be trained to handle such transitions seamlessly, ensuring that customers do not have to repeat themselves or face delays.

Wells Fargo addressed this need by training its branch and call center staff to access unified customer profiles. This approach allowed employees to provide informed support regardless of where the customer’s journey began, enhancing the overall experience. - Equipping Employees with Unified Tools

To deliver consistent support, employees must have access to the same real-time data and tools as digital platforms. Unified customer profiles, transaction histories, and personalized insights empower employees to resolve queries efficiently and offer tailored solutions.

DBS Bank’s investment in real-time data synchronization and employee training underscores the importance of this best practice. By providing staff with up-to-date information, the bank ensured that its employees could deliver a level of service that matched the sophistication of its digital tools.

The best practices outlined above—seamless channel integration, leveraging advanced analytics and AI, and investing in employee training—are critical for banks seeking to emulate the success of leading omnichannel banking examples. These strategies not only enhance customer satisfaction but also improve operational efficiency and build brand loyalty. By adopting these best practices, banks can position themselves as leaders in an increasingly competitive and customer-focused industry.

Common Pitfalls and How to Avoid Them

The success stories of omnichannel banking examples provide valuable insights into best practices, but they also reveal common pitfalls that can hinder the effectiveness of an omnichannel strategy. From fragmented systems to security challenges, understanding these issues and addressing them proactively is critical for financial institutions aiming to deliver seamless, customer-centric services. This section explores four major challenges and offers actionable solutions to overcome them.

Challenge: Fragmented Systems and Data Silos

One of the most significant obstacles in implementing an omnichannel banking strategy is fragmented systems and data silos. When customer information is scattered across multiple platforms and departments, it becomes difficult to provide a cohesive and personalized experience. Many omnichannel banking examples highlight the importance of overcoming this challenge to achieve success.

- Invest in Integration Platforms

To eliminate data silos, banks should invest in integration platforms, such as middleware solutions or API-driven systems, that centralize customer data. These platforms enable seamless communication between various systems, ensuring that all channels—digital and physical—have access to consistent and up-to-date information. For instance, Wells Fargo’s unified customer profile system allowed its employees across branches and digital platforms to access the same data, enhancing the customer experience. - Establish Clear Protocols for Data Sharing

Fragmented systems often arise from a lack of standardization in data sharing processes. Banks must establish clear protocols for data synchronization across departments and channels. This includes defining how and when customer data is updated and ensuring that all systems are aligned. Citibank’s focus on real-time data synchronization across its omnichannel ecosystem is an excellent example of how standardization can eliminate silos and improve service consistency.

Challenge: Overlooking Physical Channels

While digital banking has gained prominence, physical branches remain an essential touchpoint for many customers, particularly for complex transactions or personalized advice. Overlooking physical channels can result in a fragmented experience, as customers often expect the same level of convenience and integration as digital platforms. Successful omnichannel banking examples illustrate the importance of aligning physical branches with digital efforts.

- Enhance In-Branch Experiences with Digital Tools

Banks can modernize their branches by incorporating digital tools like kiosks, tablets, and augmented reality (AR). These technologies not only streamline in-branch processes but also align the physical experience with the convenience of digital channels. For example, DBS Bank’s transition to paperless branches involved integrating digital kiosks and e-forms, significantly improving the efficiency of in-branch services while maintaining their relevance in a digital-first era. - Foster Collaboration Between Physical and Digital Teams

To create a unified service model, banks must ensure that their physical and digital teams work collaboratively. This means integrating customer data across channels so that branch staff have access to the same information as digital platforms. HSBC exemplified this by aligning its global operations, ensuring that customers received consistent service whether they interacted online or in a branch.

Challenge: Security and Privacy Concerns

With the rise of omnichannel banking, the volume of customer data being collected and shared across multiple platforms has increased significantly. This has made security and privacy a top concern for financial institutions. Omnichannel banking examples emphasize the need for robust measures to protect customer information and comply with regulations.

- Implement Robust Encryption and Compliance Measures

Protecting customer data requires strong encryption protocols and adherence to global data protection regulations, such as GDPR in Europe or CCPA in California. Banks must ensure that all systems, whether digital or physical, meet these standards. For instance, Wells Fargo’s commitment to data security involved adopting advanced encryption methods to safeguard sensitive customer information across its channels. - Regular Audits and Employee Training

Security is not just about technology; it also involves people. Banks should conduct regular audits to identify vulnerabilities and implement training programs for employees to reinforce best practices in data privacy. Educating staff on topics such as phishing scams and secure data handling ensures that human error does not compromise the integrity of the system.

Challenge: Complexity of Implementation

Implementing an omnichannel strategy is a complex process that requires significant resources and coordination. The risk of misalignment, delays, or operational disruptions can deter banks from fully committing to this transformation. However, successful omnichannel banking examples demonstrate that strategic planning and partnerships can mitigate these risks.

- Adopt a Phased Implementation Strategy

Instead of attempting to overhaul all channels simultaneously, banks should adopt a phased approach. This allows them to focus on high-impact areas first, gather feedback, and refine their strategies before expanding to additional touchpoints. For example, Bank of America began its omnichannel journey by enhancing its mobile platform with the introduction of Erica, an AI-powered assistant, before integrating other channels. This phased rollout minimized disruptions and ensured a smooth transition. - Partner with Experienced Technology Providers

Collaborating with technology providers that specialize in omnichannel solutions can streamline the implementation process. These partners bring expertise in system integration, scalability, and customer experience design, reducing the burden on the bank’s internal teams. DBS Bank’s success in leveraging advanced technologies for its omnichannel strategy highlights the value of partnering with experienced providers to achieve operational excellence.

The challenges of implementing an omnichannel banking strategy—fragmented systems, overlooked physical channels, security concerns, and complexity—are significant but not insurmountable. The solutions outlined in this section, inspired by successful omnichannel banking examples, provide a roadmap for overcoming these obstacles. By investing in integration platforms, modernizing physical branches, prioritizing data security, and adopting a phased implementation strategy, banks can deliver seamless and secure customer experiences across all channels. Addressing these pitfalls proactively ensures that financial institutions remain competitive in a rapidly evolving digital landscape.

Criteria for Successful Omnichannel Banking

In analyzing various omnichannel banking examples, it becomes evident that achieving success in this space requires meeting specific criteria. These benchmarks ensure that banks not only provide seamless, integrated customer experiences but also optimize operations and adapt to the rapidly evolving financial landscape.

Customer-Centric Approach

A customer-centric approach is a cornerstone of successful omnichannel banking strategies. Across various omnichannel banking examples, institutions that prioritize understanding and meeting customer needs stand out as leaders in the industry. By focusing on customer behavior, convenience, and feedback, banks can design experiences that resonate with their clientele and foster long-term loyalty.

Understanding and Adapting to Customer Behavior and Preferences

To create an effective omnichannel strategy, banks must first understand how customers interact with their services. This involves analyzing behavior across multiple touchpoints, including mobile apps, online platforms, branches, and ATMs. Successful omnichannel banking examples demonstrate that tailoring services to customer preferences enhances satisfaction and engagement.

- Customer Behavior Analysis: By leveraging data analytics, banks can identify patterns and trends in customer behavior. For instance, a bank might discover that younger demographics prefer mobile-first solutions, while older customers may still value in-person interactions at branches. Recognizing these preferences allows banks to allocate resources effectively and offer services that align with customer habits.

- Adaptive Strategies: Customer preferences are not static; they evolve with technological advancements and market dynamics. Banks must remain flexible and continuously adapt their strategies to meet changing expectations. Citibank’s use of artificial intelligence to personalize financial advice based on real-time data is a notable omnichannel banking example of this adaptability.

Prioritizing Customer Convenience

Convenience is a key driver of customer satisfaction in banking. Omnichannel banking examples highlight the importance of offering consistent and accessible services across all channels. Customers should be able to move seamlessly between touchpoints without experiencing disruptions or redundancies.

- Consistency Across Channels: Banks must ensure that customers have a uniform experience, whether they interact via mobile apps, online portals, or physical branches. Consistency in branding, messaging, and functionality builds trust and reinforces the bank’s reliability. For example, DBS Bank achieved this by designing a unified user experience that integrated its mobile app, branch services, and ATMs.

- Accessibility and Ease of Use: Services must be intuitive and easy to access, regardless of the customer’s technical proficiency. Features such as real-time account synchronization, simplified navigation, and quick access to support enhance convenience. Wells Fargo exemplifies this criterion by offering self-service tools and proactive support through its mobile and online platforms.

Collecting and Acting on Customer Feedback

Customer feedback is an invaluable resource for refining the omnichannel experience. Successful omnichannel banking examples demonstrate that proactively seeking and acting on feedback can identify pain points and opportunities for improvement.

- Feedback Collection Mechanisms: Banks can use surveys, focus groups, and in-app feedback forms to gather insights directly from customers. Additionally, analyzing customer interactions and complaints provides valuable information about areas that require attention.

- Iterative Improvement: Acting on feedback is as important as collecting it. Leading banks continuously refine their services based on customer input, ensuring that their offerings remain relevant and effective. HSBC’s ongoing enhancements to its global transaction platform, informed by customer insights, highlight the role of feedback in driving innovation.

The customer-centric approach is a critical criterion for successful omnichannel banking. By understanding customer behavior, prioritizing convenience, and actively incorporating feedback, banks can create experiences that meet and exceed customer expectations. The lessons from leading omnichannel banking examples underscore the importance of placing the customer at the heart of every strategy, ensuring long-term success in an increasingly competitive financial landscape.

Seamless Integration of Touchpoints

Seamless integration of touchpoints is a defining feature of successful omnichannel banking. Customers today interact with banks through various platforms—mobile apps, online portals, physical branches, and ATMs. The most effective omnichannel banking examples demonstrate that unifying these touchpoints creates a consistent, personalized, and efficient customer experience. Below, we explore the critical components of seamless integration and how they contribute to the success of omnichannel banking strategies.

Ensuring a Unified Experience Across Touchpoints

The ability to provide a unified experience across in-branch services, mobile apps, online banking, and ATMs is a hallmark of successful omnichannel banking examples. Customers expect continuity when they move between these channels, with their data, preferences, and transaction history readily accessible wherever they interact.

- Consistency in Service Delivery: Whether a customer starts a loan application on a mobile app, continues it at a branch, or completes it online, the process should be smooth and uninterrupted. Disjointed experiences, such as having to re-enter information or explain needs repeatedly, can frustrate customers and erode trust. Citibank’s omnichannel strategy exemplifies this criterion by allowing customers to transition seamlessly between channels while maintaining a consistent experience.

- Integration of Physical and Digital Channels: In-branch services should complement digital interactions rather than operate as isolated silos. For instance, a customer using a bank’s ATM should see the same account information and transaction options available on their mobile app. Wells Fargo is a prime omnichannel banking example of this approach, having integrated its digital and physical channels to provide a cohesive experience across touchpoints.

Implementing a Single Customer View

A single customer view (SCV) is essential for synchronizing data across all channels in real time. By consolidating customer information into a centralized system, banks can ensure that every touchpoint provides accurate and up-to-date data, enhancing the customer experience.

- Real-Time Data Synchronization: SCV enables real-time updates to customer profiles, ensuring that any action taken on one channel is immediately reflected across others. For example, if a customer updates their contact information on the mobile app, branch staff and call center representatives should instantly have access to the updated details. HSBC’s global transaction platform leverages this capability to deliver a consistent and reliable experience across its network.

- Personalized Interactions: A single customer view also allows banks to personalize interactions by providing staff and digital platforms with a complete picture of the customer’s history, preferences, and needs. Proactive support, such as recommending relevant financial products or offering timely advice, becomes possible when data is unified. Bank of America’s use of Erica, its AI-driven assistant, showcases how SCV can enable highly personalized and efficient customer interactions.

Providing Consistent Branding and Communication

Consistent branding and communication are critical for reinforcing trust and reliability in an omnichannel banking strategy. Customers should feel confident that they are interacting with the same institution, regardless of the channel they use.

- Uniform Branding Across Platforms: From the design of mobile apps and online portals to the appearance of ATMs and branch interiors, branding should be cohesive and recognizable. This consistency reinforces the bank’s identity and reassures customers that they are receiving the same quality of service everywhere. DBS Bank exemplifies this criterion by delivering a unified user experience across all its channels, ensuring that customers feel connected to the brand at every touchpoint.

- Standardized Communication: Messaging should be aligned across all channels, whether it’s notifications sent via email, SMS alerts, or information provided by branch staff. Standardized communication reduces confusion and reinforces the bank’s commitment to transparency and professionalism. Wells Fargo’s approach to omnichannel banking includes clear and consistent messaging across its digital and physical platforms, building trust and clarity in customer interactions.

Seamless integration of touchpoints is a cornerstone of successful omnichannel banking strategies. By unifying in-branch services, mobile apps, online banking, and ATMs, banks can provide a consistent and personalized experience that meets customer expectations. Real-time data synchronization through a single customer view further enhances this integration, enabling accurate and timely interactions. Additionally, consistent branding and communication across channels ensure that customers feel connected to the institution, regardless of how they engage.

These elements, as seen in leading omnichannel banking examples like Citibank, HSBC, and Wells Fargo, highlight the importance of seamless touchpoint integration in creating a customer-centric and efficient banking ecosystem. Banks aiming to succeed in the omnichannel landscape must prioritize these criteria to deliver a superior experience that fosters trust, satisfaction, and loyalty.

Advanced Technologies

The integration of advanced technologies is pivotal in achieving a successful omnichannel banking strategy. The most effective omnichannel banking examples illustrate how financial institutions leverage artificial intelligence (AI), machine learning (ML), predictive analytics, and innovative tools like biometric authentication and blockchain to deliver personalized, secure, and efficient services. These technologies not only enhance customer experiences but also streamline operations, making them indispensable for banks aiming to remain competitive in a rapidly evolving industry.

Leverage AI and Machine Learning to Predict Customer Needs

AI and machine learning are transformative tools that enable banks to understand and predict customer needs with unparalleled precision. By analyzing vast amounts of data, these technologies provide actionable insights that drive personalized solutions.

- Personalized Financial Solutions: AI and machine learning allow banks to offer tailored recommendations based on individual customer behavior, preferences, and financial goals. For example, a bank might analyze spending patterns to suggest budgeting tools or recommend investment opportunities aligned with a customer’s risk tolerance. Citibank’s use of AI to provide personalized financial advice is a prime omnichannel banking example, demonstrating how these technologies enhance customer satisfaction and engagement.

- Proactive Support and Alerts: AI-driven tools can anticipate customer needs and deliver proactive alerts. For instance, a customer nearing their credit card limit might receive a real-time notification suggesting a balance transfer option or a payment reminder. This level of proactive support builds trust and strengthens the customer-bank relationship.

Utilize Predictive Analytics to Anticipate Customer Behavior

Predictive analytics is a cornerstone of advanced omnichannel banking strategies. By analyzing historical data and behavioral trends, banks can anticipate customer actions and optimize engagement strategies across all channels.

- Enhancing Customer Engagement: Predictive analytics enables banks to identify opportunities for engagement before the customer takes action. For example, a customer consistently using their mobile app for bill payments might be offered an automated payment setup feature, streamlining their experience. HSBC’s predictive analytics capabilities, which inform its global transaction platform, exemplify how anticipating customer behavior can lead to improved service delivery and satisfaction.

- Improving Marketing Effectiveness: Banks can use predictive analytics to refine their marketing efforts, ensuring that customers receive offers and promotions that are relevant to their needs. For example, customers with upcoming travel plans might be targeted with foreign exchange or travel insurance offers. This targeted approach not only increases conversion rates but also enhances the customer experience.

Adopt Cutting-Edge Tools Like Biometric Authentication and Blockchain

Advanced tools like biometric authentication and blockchain technology are redefining security and operational efficiency in omnichannel banking. These innovations ensure that customer interactions are both secure and seamless, addressing some of the most critical concerns in modern banking.

- Biometric Authentication for Enhanced Security: Biometric tools such as fingerprint scans, facial recognition, and voice identification add a layer of security that is difficult to breach. These technologies are also convenient for customers, eliminating the need for passwords or security questions. Bank of America’s integration of biometric authentication into its mobile app is a notable omnichannel banking example, showcasing how advanced security measures can simultaneously improve usability.

- Blockchain for Secure Transactions: Blockchain technology provides a decentralized and tamper-proof ledger for financial transactions, ensuring transparency and security. Banks adopting blockchain for cross-border payments or digital contracts can offer faster, more reliable services to their customers. While blockchain is still emerging in mainstream banking, its potential to enhance omnichannel strategies by enabling seamless and secure operations is immense.

Advanced technologies are essential for the success of any omnichannel banking strategy. From leveraging AI and machine learning to predict customer needs, to utilizing predictive analytics for optimizing engagement strategies, and adopting cutting-edge tools like biometric authentication and blockchain, these innovations drive personalization, security, and efficiency.

Leading omnichannel banking examples, such as those from Citibank, HSBC, and Bank of America, demonstrate the transformative impact of advanced technologies on customer experience and operational effectiveness. By embracing these tools, banks can stay ahead of industry trends, deliver exceptional value to customers, and build a robust foundation for future growth in a competitive financial landscape.

Personalization

Personalization is at the core of successful omnichannel banking strategies. Customers today expect tailored experiences that align with their individual needs, preferences, and financial goals. Leading omnichannel banking examples reveal that the ability to deliver personalized services not only enhances customer satisfaction but also strengthens loyalty and trust. By leveraging customer data, dynamic messaging, and consistent personalization across touchpoints, banks can create meaningful interactions that resonate with their customers.

Use Customer Data to Create Tailored Offers, Services, and Recommendations

A deep understanding of customer behavior and preferences is essential for providing personalized experiences. Successful omnichannel banking examples show how banks utilize data analytics to craft customized offers, services, and recommendations that address individual customer needs.